Hyper-Personalized Banking: A Data-Driven Approach

Hyper-personalized banking, powered by cutting-edge AI and streaming analytics, is transforming customer experience in financial services – boosting loyalty, revenue, and competitive edge.

Today’s consumers aren’t comparing their banking experience to other banks–they’re comparing it to the seamless, personalized interactions they get from Amazon and Netflix. They now expect the same level of relevance and responsiveness from financial institutions. Traditional segmentation, i.e. grouping customers by broad demographics or product types, no longer meets the mark. Customers want real-time, tailored experiences that reflect their unique needs and behaviors. Generic marketing messages and one-size-fits-all outreach simply don’t resonate.

The good news? Financial services firms now have the data, tools, and technology to deliver hyper-personalization at scale. With real-time data, advanced analytics, and Generative AI (GenAI), organizations can move beyond static segments to offer dynamic, individualized experiences from personalized product recommendations to proactive financial guidance.

That said, adoption takes time. Financial institutions are understandably cautious, doing their best to balance innovation with regulatory compliance, data privacy, and risk management. However, for those willing to invest, the long-term payoff in customer loyalty and competitive differentiation is substantial.

The ROI of Hyper-Personalized Banking

Hyper-personalization in consumer banking consistently delivers strong ROI. It can reduce customer acquisition costs by up to 50% and increase revenue by 5-15%. According to McKinsey, 71% of consumers now expect personalized interactions, and 76% express frustration when these expectations aren’t met.

The alignment between business value and customer demand makes investment in hyper-personalized banking experiences a strategic imperative. Beyond improved targeting and operational efficiency, hyper-personalization drives higher cross-sell and upsell rates through more relevant product offerings. By moving past traditional segmentation, banks can better anticipate customer needs, strengthen relationships, and boost customer lifetime value.

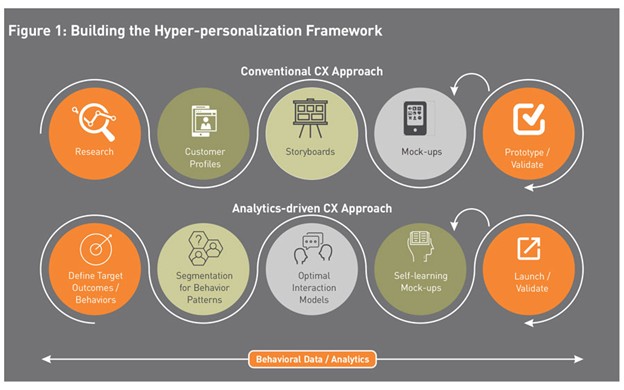

Image courtesy of walkme.com

What is Hyper-Personalization in Banking?

Hyper-personalization spans far beyond traditional demographic segmentation. Instead of static personas that group customers by age, income, or product type, hyper-personalization tailors services, offers, and communications at the individual level, based on real-time behaviors, preferences, and needs. It’s about delivering a narrow, personally relevant message, through the most engaging channel, at exactly the right moment, all predicted by this new level of data.

This level of precision is made possible by a combination of advanced technologies, including:

Generative AI to create dynamic, personalized content and responses at scale

Real-time behavioral data to track and respond to customer actions as they happen

Predictive analytics and machine learning to anticipate needs and recommend next-best actions

Omnichannel delivery to ensure consistency across digital, mobile, in-branch, and contact center experiences

In practice, hyper-personalized banking can take many forms:

A customer receives real-time fraud alerts based on unusual spending behavior

A banking app offers custom product recommendations aligned with recent life events or financial goals

A chatbot provides personalized financial advice, drawing from transaction history and savings patterns

These experiences not only improve customer satisfaction–they build trust and long-term loyalty in a highly competitive market.

Data Foundations that Power Personalization

Hyper-personalized banking relies on robust data foundations. Understanding the critical data sources and enablers or success is essential for delivering personalized experiences at scale.

Critical Data Sources:

Transactional Data: The foundation of analytics in this industry, this includes data from customer transactions like purchases, payments, and transfers. Transactional data provides insights into spending habits, financial health, and product usage. Technologies like Apache Kafka and AWS Kinesis can be used to stream transactional data in real-time.

Mobile and Web Behavior Analytics: Tracking customer interactions on mobile apps and websites allows understanding of their preferences, behaviors, and engagement patterns. Tools like Google Analytics, Adobe Analytics, and Mixpanel can capture this data. Integration with customer data platforms (CDPs) like Segment or Tealium can further enhance data collection and analysis.

CRM and Customer Service Interactions: Customer Relationship Management (CRM) systems like Salesforce and Microsoft Dynamics, along with customer service platforms like Zendesk, capture valuable information about customer inquiries, feedback, and support history. This helps to further personalize communication and service offerings.

Third-Party Enrichment Sources: External data sources, such as credit bureaus (e.g., Experian, Equifax, TransUnion) and open banking APIs (e.g., Plaid, Yodlee), provide additional context and validation. These sources enrich internal data, offering a more comprehensive view of the customer.

Enablers of Success:

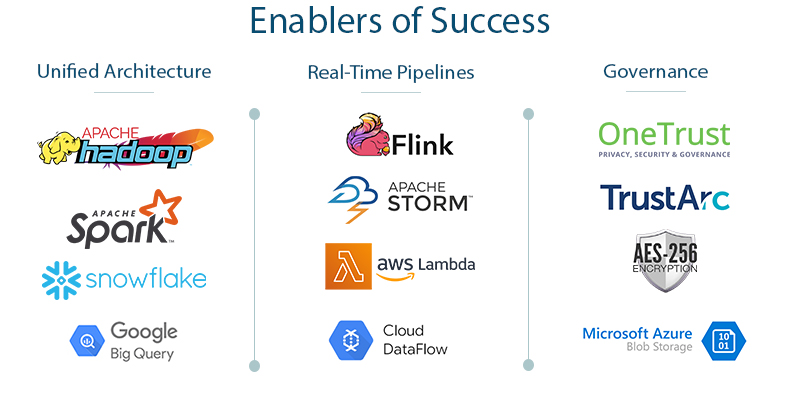

Clean, Unified Data Architecture: A well-structured data architecture ensures that data from various sources is integrated, cleaned, and standardized. Technologies like Apache Hadoop, Apache Spark, and data warehousing solutions like Snowflake or Google BigQuery can be used to create a unified data architecture.

Real-Time Data Pipelines: Real-time data processing enables immediate insights and actions. Tools like Apache Flink, Apache Storm, and cloud-based solutions like AWS Lambda and Google Cloud Dataflow ensure that data is continuously updated and available for analysis, allowing for timely and relevant personalization.

Consent and Privacy Governance: In the financial services sector, maintaining customer trust is paramount. Robust consent and privacy governance frameworks ensure that data is used ethically and complies with regulatory requirements. Tools like OneTrust and TrustArc can help manage consent and privacy compliance, while encryption technologies like Advanced Encryption Standard (AES) and secure data storage solutions like Azure Blob Storage ensure data protection.

Regardless of which technology stack you choose, it’s critical for it to integrate all of your applicable data sources so that real-time updates are available to the customer.

Enjoying this insight?

Sign up for our newsletter to receive data-driven insights right to your inbox on a monthly basis.

Real-time analytics is a true game changer for financial services, enabling organizations to deliver contextual, relevant offers to the customer at the exact moment of need. Not only does this capability enhance customer experience (CX), but it also drives loyalty and product update. By leveraging real-time data, financial institutions can anticipate customer needs and respond with precision.

Key Benefits of Real-Time Analytics:

Contextual Offers: Delivering personalized offers and recommendations based on real-time data ensures that customers receive relevant information when they need it most.

Increased Loyalty: By meeting customer needs promptly and accurately, financial institutions can build stronger relationships and foster customer loyalty.

Higher Product Adoption: Timely, relevant offers are more likely to be accepted, leading to increased product adoption and revenue growth.

Potential Opportunities:

GenAI-Powered Chatbots: AI-driven chatbots can deliver real-time, personalized financial information, suggestions, and support, using customer context and behavioral data to tailor responses instantly.

Fraud Detection and Prevention: By monitoring transactions in real-time, banks can detect suspicious spending patterns and immediately alert the customer of potentially fraudulent purchases, mitigating financial losses and protecting the customer.

News Aggregation: AI can aggregate and filter financial news in real time, highlighting only the most relevant updates tied to a client’s holdings in the form of prompt alerts and daily summaries. By surfacing critical developments – earnings reports, regulatory changes, geopolitical events, etc. – AI also helps Portfolio Managers make timely, informed decisions.

Low Balance Alerts & Product Suggestions: Financial apps can send real-time alerts that anticipate customer needs. For example, if a customer’s account balance is low, the app can suggest transferring funds from a savings account or offer a short-term personal loan.

Location-Based Promotions: Using geolocation data, banks can provide location-based offers, such as nearby ATMs locations (e.g., with a $0 withdrawal fee) or dining perks at partner restaurants. This enhances customer experience by providing value-added services based on their current location.

Of course, it’s easy to look at the hypotheticals, but where does the rubber meet the road in the industry? Some of finance’s biggest heavyweights have been investing in AI and Machine Learning to fuel hyper-personalization for years, long before AI became headline news.

Capital One leaned strongly into hyper-personalization by leveraging AI to build their intelligent assistant, Eno. This innovative chatbot allows Capital One to send personalized notifications and offers and can even help with managing personal finances. The innovation factor comes from the approach – Capital One partnered with retailers to generate geo-specific prompts by featuring offers when a customer is near one of the partnered retailers.

In this article from IBM, AI is clearly part of the financial service industry’s roadmap. Their 2025 Global Outlook for Banking and Financial Markets calls out the expected challenges and opportunities presented by AI. Regardless, IBM, like many others, believes that the future of banking is AI-driven.

By integrating real-time analytics into their operations, financial institutions can stay ahead of customer expectations and deliver exceptional, personalized experiences.

UI and CX: Making Data-Driven Personalization Feel Human

Digital UX in exemplifies the power of real-time, hyper-personalized banking experiences that today’s consumers demand. Emotionally intelligent engagement, through thoughtful tone, timing, and context, further elevates the experience, ensuring that each customer journey is met with relevance, empathy, and authenticity.

Emotionally intelligent engagement enhances CX and UI. Banking exemplifies this by aligning key humanized driven elements such as tone, timing, and context with the customer’s emotional state and intent, in a real-time fashion. This creates interactions that feel deeply personal and relevant–even if powered by technology.

To make data-driven personalization feel human, businesses must go beyond demographics to interpret behavioral signals and emotional cues, like recognizing a banking customer who frequently checks mortgage rates and recently increased savings account contributions, then sending a personalized message that says, “We see you’re planning ahead. Here’s a tailored guide to first-time homebuying and low-interest mortgage options just for you,” using a supportive, empathetic tone that aligns with the customer’s financial goals and journey.

Authenticity is achieved when personalization mirrors real human understanding.

Implementation Considerations for Hyper-Personalized Banking

Implementing hyper-personalized banking and other financial services requires careful planning, as there will inevitably be challenges to face, and key criteria must be met in order to reap the benefits..

Challenges to Anticipate:

Legacy Systems and Siloed Data: Many financial institutions operate on legacy systems that are not designed to handle the demands of modern data processing and integration. These systems often result in siloed data, making it difficult to create a unified view of the customer. Overcoming this challenge requires investing in modern data infrastructure and integration solutions.

Regulatory Scrutiny Around Data Use and Privacy: Financial institutions are subject to stringent regulations regarding data use and privacy. Compliance with regulations such as GDPR, CCPA, and other data protection laws is critical. Institutions must ensure that their data practices are transparent, secure, and compliant with all applicable regulations.

Aligning Personalization Implementation with Business Goals: It’s essential to ensure that personalization efforts are aligned with broader business objectives. This means setting clear goals for personalization initiatives and measuring their impact on key business metrics such as customer satisfaction, engagement, and revenue growth.

Success Factors:

Cross-Functional Collaboration: CX, data science, compliance, and product teams must work together from strategy to execution.

Clear Governance Model: Defined roles, policies, and oversight ensure data is used responsibly and effectively.

Iterative Rollout with Measurable Impact: Start small (pilot projects), test continuously, and scale based on performance and insights.

Like most other technology-heavy projects, the secret sauce is keeping a focus on detail while never forgetting the bigger picture of delivering exceptional customer experiences.

Final Thoughts: Start Small, Learn Fast

Not every solution needs to be fully automated from the start. Begin with a single journey, like customer onboarding, and focus on delivering personalized experiences. Test, iterate, and gradually expand your personalization maturity.

Hyper-personalization doesn’t have to feel daunting, especially with RevGen’s expert guidance by your side. Whether you are hoping to build on top of your current data strategy or needing to modernize your architecture to enable AI and Advanced Analytics, we can help. Contact us today to speak to one of our personalization experts.

Alex Champagne is a Senior Consultant at RevGen specializing in data storytelling and BI development. He is passionate about helping organizations identify hidden insights in their data and enhancing the ways they engage with their customers and colleagues.

Stephanie Caravajal is a Senior Manager at RevGen. She helps organizations understand how to increase customer value by understanding the customer needs and align digital enhancements by applying an overall digital architecture.

AI initiatives succeed or stall based on the quality of the data behind them. The Databricks Data Intelligence Platform is built from the foundation up to address exactly that.

The path to agentic AI isn't a leap—it's a climb built on data quality foundations. Proactive monitoring transforms operations today while enabling autonomous capabilities tomorrow.